Going Full Brazilian: Why Brazilian Stocks Are Super Undervalued Right Now

With Donald Trump’s second nomination, US stocks are soaring, with index funds reaching their all-time highs. Forecasts by Goldman Sachs and Morgan Stanley have indicated that this strength will continue through 2025, rising by at least 10% by the end of 2025.

However, at such inflated prices, one may be left baulking at acquiring one the ‘Magnificent Seven’ at current prices; or even worse — getting caught in the downside potential of a of a market crash. While prices might eventually bounce back, well as the saying goes — time is money.

So can we still find value in today’s overheated market? If you’d like to diversify your holdings and take a punt on growth, then head down to the land of Samba, bikinis and football: Brazil.

How undervalued are Brazilian stocks?

Looking at the statistics above, US stocks are currently highly overvalued, represented by its high Price-to-earnings (P/E ratio).

P/E ratios are earnings taken from the trailing twelve months (TTM) performance of each country’s equity index. The lower the number, the more undervalued it is.

In comparison, Brazil sits near the bottom — just under China — together with Polish, Austrian, Colombian, Greek and Turkish stocks.

A further look at the stock country performance in the ‘big countries’ shows that Brazil sits rock bottom, just below China.

So why Brazil stocks?

Many Brazilian stocks are listed on the NYSE, have huge market caps, and are diversified in different industries. Let’s do a quick analysis of other undervalued countries with P/E ratios below Brazil’s: Poland, Austria, Colombia, Greece and Turkey.

- Poland — no stocks listed.

- Austria — no stocks listed.

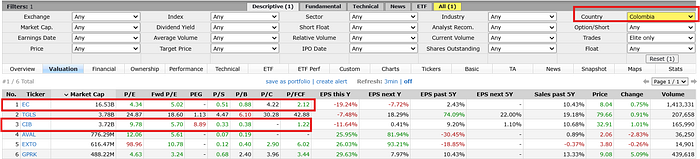

- Columbia — 6 stocks listed. Stocks with ‘acceptable’ price ratios and market caps (above 2B) are EC or CIB (red boxes). However, growth potential for the next few years is weak for this country right now as indicated by its high/missing PEG ratios.

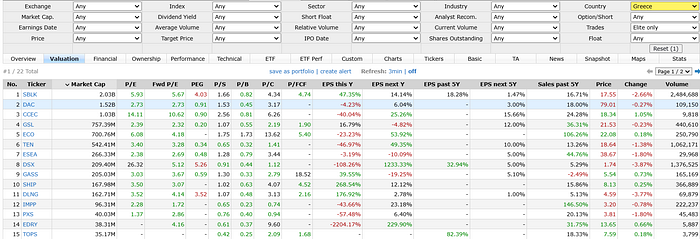

- Greece — 22 stocks listed. Lots of great bargains. However, most are small cap companies (<2B market cap) in the marine shipping sector — which might expose you to higher risk when investing.

- Turkey — 3 stocks listed. Only stock with a significant market cap worth considering is TKC.

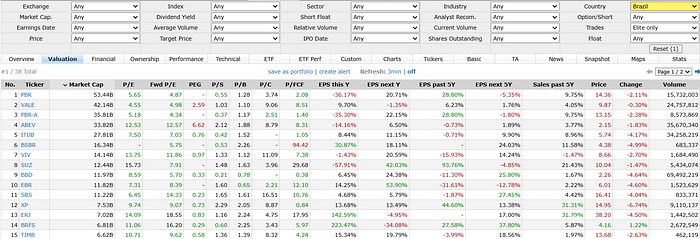

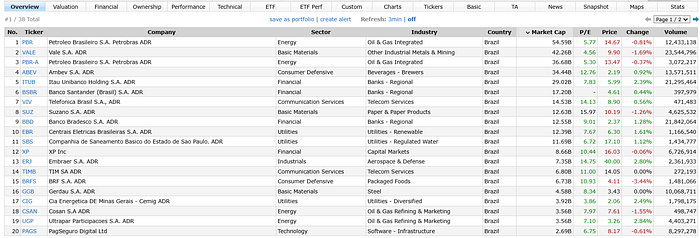

- Brazil — 38 stocks listed, 11 large cap stocks (>10B market cap), and a good mix of highly undervalued stocks from a host of various industries to choose from.

Why are Brazilian stocks priced so low?

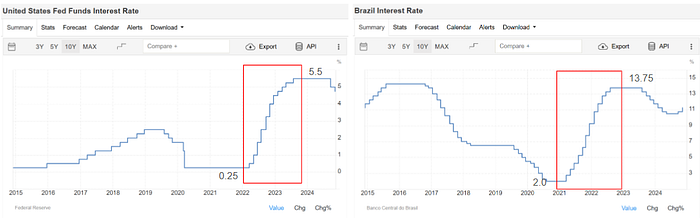

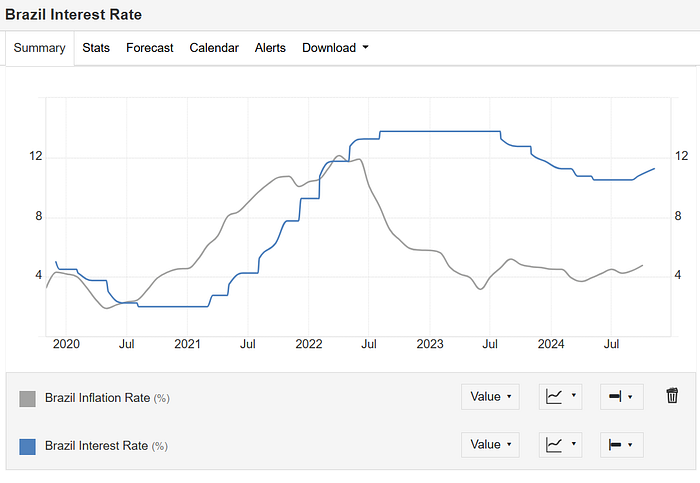

Brazilian stocks have taken a beating. In a post-COVID world where interest rates were increased to combat inflation (the US raised interest from 0.25 to 5.5 by 4.25 points), Brazil did so by a whopping 11.75 points (nearly 3 times the US) to 13.75 points.

From July 2024 to August 2024, Banco Central do Brasil (Brazil’s central bank — BCB ) eased up interest rates allowing for some economic growth — but inflation reared its ugly head once again.

Since then, BCB has hiked up its interest rates by another 0.75 points while the US Federal Reserve (Feds) cut its rates by 0.75 points, sending Brazilian stocks to plumet. The Fed rate cut and Donald Trump’s nomination has led to a strong US economy to the point where the Feds are delaying more rate cuts as promised.

On the other hand, analysts have projected that Brazil’s central bank will continue raising interest rates through July next year, with the rate projected to surpass 14%. High interest rates are of course, detrimental to economies as they discourage spending.

Should you take a punt on Brazil?

If you’d like to make a contrarian play, Brazilian stocks are perfect for it. There are a host of stocks that are currently undervalued, have huge potential growth, huge market caps, and with many industries to choose from.

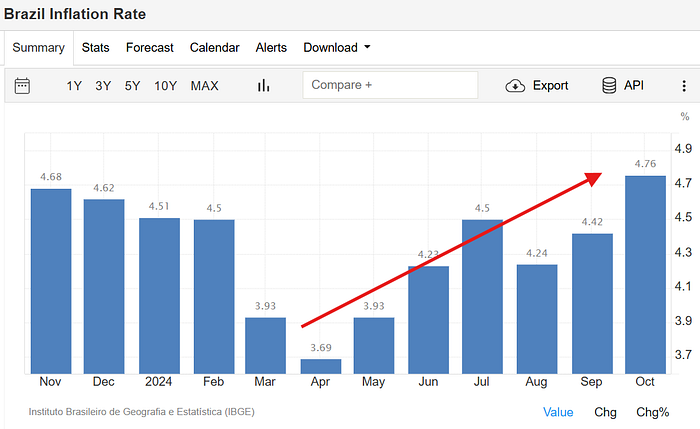

However, Brazil’s stock performance also boils down to its inflation rate moving into 2025.

Despite Brazil’s first 0.25 point interest rate hike in September, inflation in October still increased. This led BCB to institute a second 0.5 point interest rate hike on November 6. Brazilian stock performance will depend on November and December’s inflation results.

Historically, judging from past performances, Brazil’s inflation rates tend to decrease slightly towards year end. In 2020, November — December saw a slight decrease in inflation, 2021 a rise in inflation, 2022 a fall in inflation and 2023 a slight decrease in inflation.

Do note that leading into 2025, Brazilian President Luiz Inacio Lula da Silva has set an inflation target of 3% — with a tolerance range of plus or minus 1.5 percentage points. This means that BCB may continue increasing interest rates if inflation continues to be persistently high.

What are some undervalued Brazilian stocks right now?

Now that we’ve analyzed that microeconomic factors of Brazil, let’s find some undervalued Brazilian stocks.

Here are some metrics that I will be looking at:

- Price ratios

- Profitability

- Intrinsic value

Price ratios

Price ratios are great for comparing stocks within their industry. Some ratios that can be used includes:

- Price-to-Earnings (P/E): Measures company’s profits

- Forward P/E: Measures company’s profits for next year

- Price-to-Earnings-Growth (PEG): Measures company’s profits for next 1–3 years

- Price-to-Book (P/B): Measures company’s assets to liabilities

- Price-to-Free-Cash-Flow (P/FCF): Measures company’s ability to generate cash over time

*Always remember, the lower the price ratio, the better.

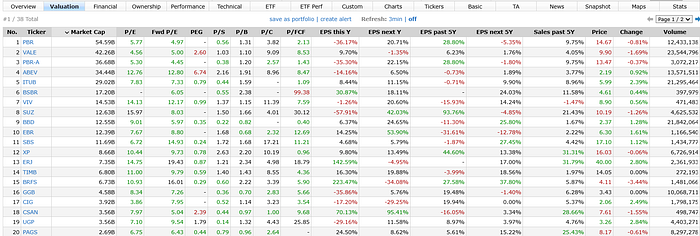

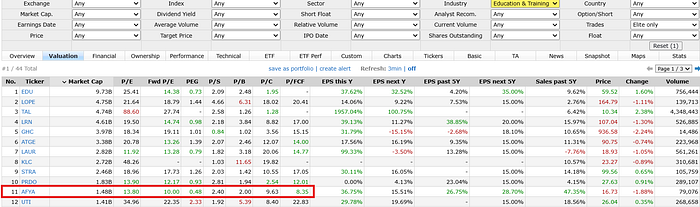

FinViz is a free screener that labels its metrics according to color. So green means better than industry average (undervalued), black means around industry average, red means worse than industry average (overvalued).

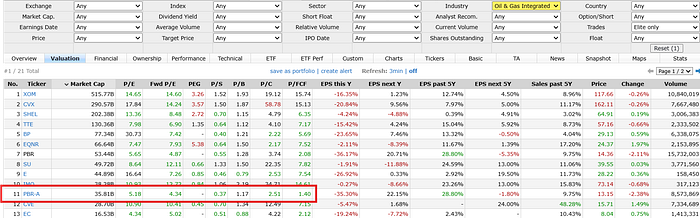

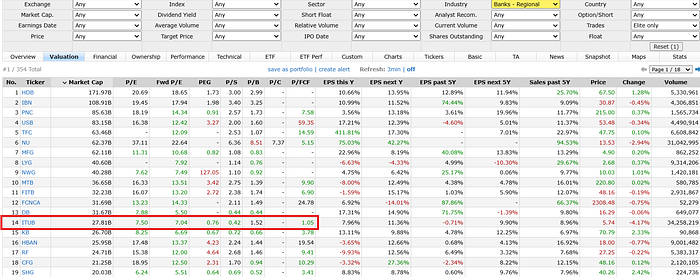

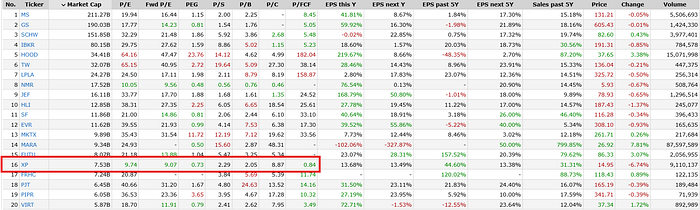

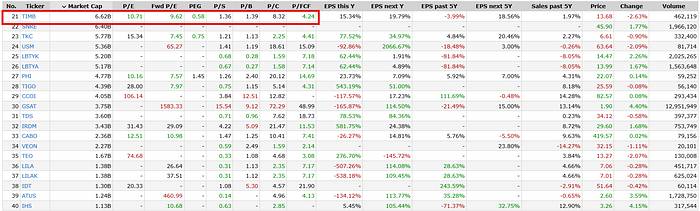

Let’s take a look at Brazil’s stocks in the screener above. From this list, stocks with good P/E and P/FCF ratios that stand out are PBR, VALE, VIV, ITUB, BBD, XP, TIMB, ASAI & AFYA.

Let’s list them according to industries.

- VALE (42.7B) — Other Industrial Metals & Mining

- PBR-A* (35.81B) — Oil & Gas Integrated

- ITUB (28.35B) — Banks — Regional

- VIV (14.29B)— Telecom Services

- TIMB (6.73B) — Telecom Services

- BBD (12.60B) — Banks — Regional

- XP (8.78B)— Capital Markets

- ASAI (1.69B)— Grocery Stores

- AFYA (1.55B)— Education & Training Services

Note: PBR-A is PBR’s preferred stock, meaning you get paid dividends before common stock shareholders, but don’t get voting rights.

We want a diversified selection, so lets compare stocks that are in the same industry to see which is better. We also want growth stocks, so we will remove ASAI (grocery stores have notoriously low margins).

Competitor analysis:

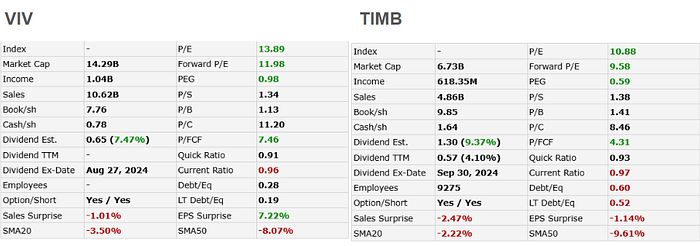

While VIV is a safer choice as it has less debt and a greater market cap than TIMB, TIMB has much better cash flow (P/FCF), growth potential (Forward P/E & PEG) and pays out consistent and higher dividends. For this reason I will pick TIMB.

Competitor analysis:

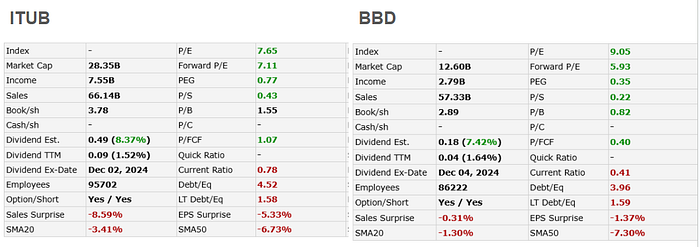

While on paper BBD has better price ratios, I am not a fan of BBD’s penny stock-like price of $2 (means there are lesser option strikes to choose from). Also, ITUB has better P/E ratio and has a higher market cap. For this reason, I will pick ITUB.

So the list we have left are:

- VALE (42.7B) — Other Industrial Metals & Mining

- PBR-A (35.81B) — Oil & Gas Integrated

- ITUB (28.35B) — Banks — Regional

- XP (8.78B) — Capital Markets

- TIMB (6.73B) — Telecom Services

- AFYA (1.55B) — Education & Training Services

Let’s do a further analysis of these stocks against their NYSE industry counterparts.

VALE

VALE is a top 3 industrial mining company in the NYSE, and has very impressive P/E, forward P/E and P/FCF values as compared to its nearest counterparts. VALE also has a very impressive dividend rate of 9.98%, making it a great dividend stock. It also has a great demand forecast, as indicated in this article.

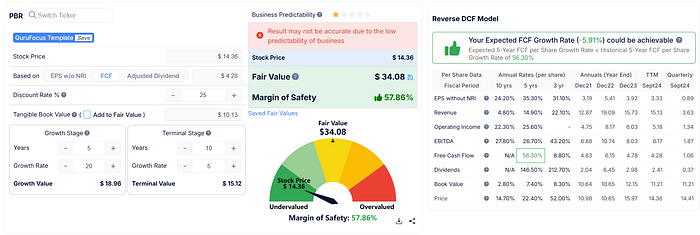

PBR-A

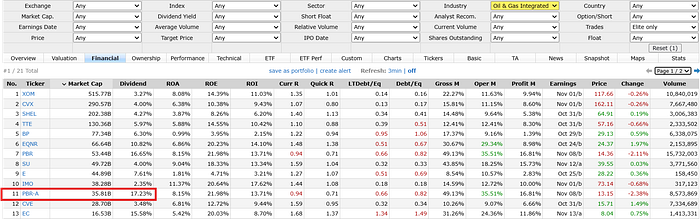

PBR-A has an excellent P/E ratio, only bettered by fellow undervalued Colombian oil stock EC, and the best P/FCF ratio. However the strength in this stock is its dividends.

PBR-A gives a whopping 17.23%, making it suitable for a long-term dividend play. However, it currently has an RSI of 50 and I would advise letting it fall more to the $12.50–$12 range before entering. Superb dividends coupled with impressive financial ratios — it doesn’t get any better than that.

ITUB

While not the best regional banking stock on this list (in my opinion SHG and PNC are better), ITUB still has a very impressive P/FCF ratio for a bank, meaning that it can generate much more cash over time — benefitting its shareholders.

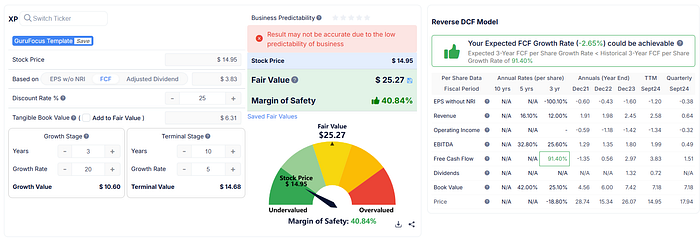

XP

The Capital Markets industry can be extremely volatile for lower cap stocks, so be careful when trading this stock.

Comparing among its top 20 competitors, the only stock that betters Brazil’s XP in terms of price ratio is Japan’s NMR. For a capital market stock, XP’s P/E ratio and P/FCF ratios are excellent shape, and is poised to grow next year. Yet another great potential growth + dividend play stock.

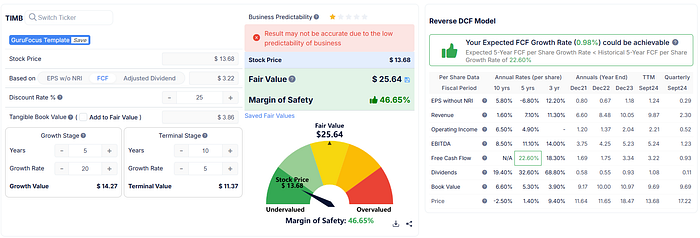

TIMB

While TIMB ranks 21 in the sector, it makes a great long play investment into Brazil’s telecom sector.

However, TIMB is not the best valued in its industry. In price ratio comparisons, UK’s Vodafone (VOD), South Korea’s KT, and USA’s Comcast (CMCSA) performs better.

However, TIMB is the only telecom stock that approaching oversold now (RSI<30), so it might be a good time to enter as compared to the others.

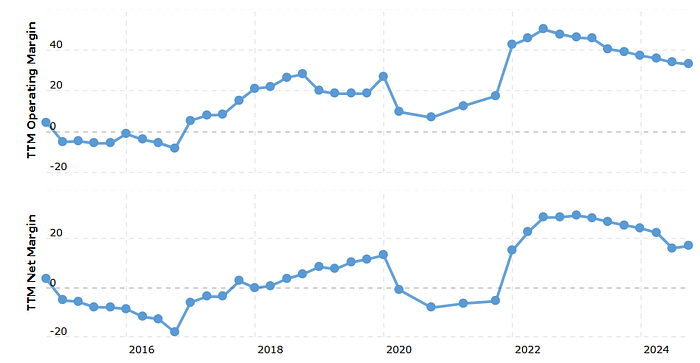

AFYA

AFYA is a curious case. It is sandwiched between PRDO and UTI — two American companies with similar market caps — but the price action couldn’t be more different. PRDO and UTI are currently at all-time highs, but AFYA’s price has been fluctuating, despite having the best valuation ratios out of the top 12 companies.

Could this be a result of Brazil’s economic microenvironment? This means that if Brazil’s inflation rates goes down, we might see AFYA shoot up higher than these two American stocks. In terms of growth, AFYA’s Forward P/E and PEG supports this claim, showing the most potential.

Profitability

Next, lets analyze the profit trend of these companies in the past 10 years. A company’s profit margin indicates its financial health and long-term viability.

- VALE (42.7B) — Other Industrial Metals & Mining

- PBR-A (35.81B) — Oil & Gas Integrated

- ITUB (28.35B) — Banks — Regional

- XP (8.78B) — Capital Markets

- TIMB (6.73B) — Telecom Services

- AFYA (1.55B) — Education & Training Services

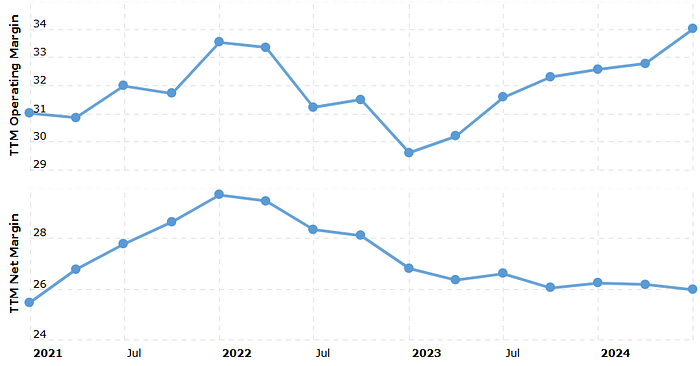

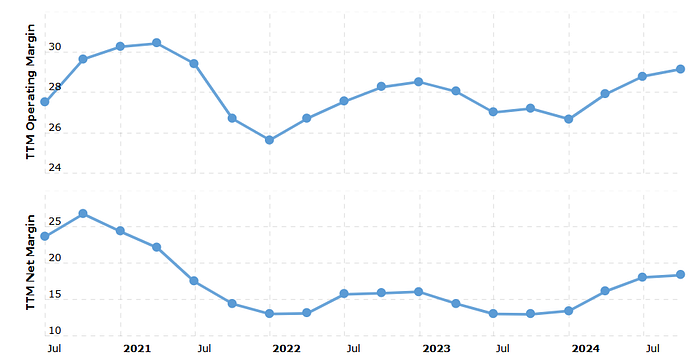

VALE

Trend analysis: With the exception of from 2014–2016 (Brazilian Economic Crisis) and the onset of COVID-19 in 2019, VALE has consistently been profitable, demonstrating its good fundamentals. While it is on a slight decline due to macroeconomic factors in the industry (all stocks are down), it has maintained an impressive 20–40% net margin over the past 3 years despite high interest rates.

PBR.A

Trend analysis: PBR has mixed net profitability over the last 10 years. However, it has maintained impressive consistent 15–28% net margin returns over the past 3 years. This is still a company that is very much affected by macroeconomic factors like the oil price war between Saudi Arabia and Russia, as highlighted between 2020 and 2021, and the Brazilian Economic Crisis.

ITUB

Trend analysis: ITUB has seen the worst and survived them all. In the past 10 years, ITUB has weathered crises like the economic recession in 2014 and COVID-19, while still remaining profitable.

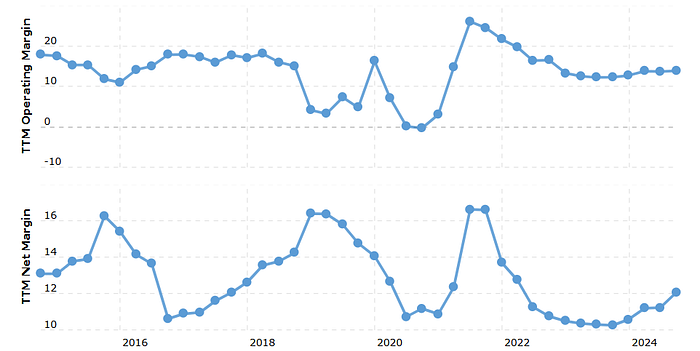

XP

Trend analysis: A relatively new stock — only 3 years old, so it hasn’t seen the worst yet. However, its operating margin is on an uptrend, signaling that XP is able to generate profit through its core operations efficiently. However, its falling net margins could be attributed to increasing taxes and interest rates.

TIMB ✅

Trend analysis: TIMB is similar to ITUB — its seen the worst and survived it all, maintaining a consistent profitability between 4 to 24%. Very impressive stock.

AFYA

Trend analysis: Similar to XP, AFYA is a relatively new stock. However it is seemingly unperturbed by Brazil’s high interest rates, seeing a growth in net and operating margin the past year. Could we see a sharp jump when interest rates are reduced? Only time will tell.

Intrinsic value

Intrinsic value uses the company’s past 5 or 10 year Free Cash Flow, discounts it, calculates its growth rate and determines how much the stock will be valued in 10 years time. A company’s growth can be measured through its intrinsic value.

Intrinsic vale is standard practice that Warren Buffet uses in finding undervalued stocks.

For simplicity’s sake, I will be using Gurufocus’ Discount Cash Flow calculator to calculate the intrinsic value of each stock.

Let’s first determine a series of presumptions.

- Discount rate: Brazil’s discount rate is currently 19% + a risk premium of 6% = 26% Discount Rate

- 10-year or 5-year FCF? Many companies do not have their 10-year FCF so we will use their 5-year FCF instead.

- Terminal growth rate will be set at 5%, which is Brazil’s current inflation rate.

Do note that we’re using extremely conservative presets here. Discount rates are normally set at 20% maximum, but we’re using 26%.

Some stocks that we’ll be analyzing have crazy FCF margins like 50% (PBR) and 90% (XP), but we’ll cap them at a sustainable 20% growth rate.

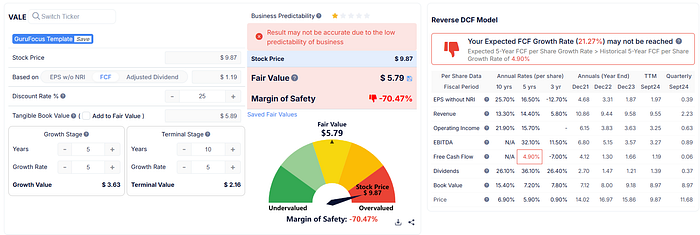

VALE

- VALE’s intrinsic value in 10 years: $5.79

- Potential increase:-58%

PBR

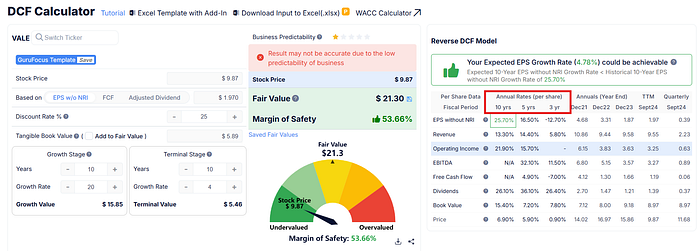

- PBR’s intrinsic value in 10 years: $34.08

- Potential increase: 237%

ITUB

- ITUB’s intrinsic value in 10 years: $34.08

- Potential increase: -177%

XP

- XP’s intrinsic value in 10 years: $25.27

- Potential increase: 169%

TIMB

- TIMB’s intrinsic value in 10 years: $25.64

- Potential increase: 188%

AFYA

- AFYA’s intrinsic value in 10 years: $14.41

- Potential increase: -14%

Conclusion

By analyzing the stocks using these 3 methods, here’s my summary:

VALE: Good for a dividend play (9.98%), however not good for accumulation now. Might want to wait for stock to fall to under $5.80 before accumulating more.

Verdict: Wait

PBR: Very undervalued right now. A stock with huge potential. Great for a dividend play as well (16.65%). However stock is very volatile and will be subjected to macroeconomic conditions, such as Trump’s trade and oil war in the future. Might want to wait for prices to fall to $13 strong support line before entering.

Verdict: Wait

ITUB: Not a growth stock. Has the ability to make consistent profits, but not worth holding in Brazil’s current economic landscape. If you want dividends, then PBR is a better play for growth and dividends or you can consider other banking stocks from other countries.

Verdict: Don’t buy

XP: Potential growth stock, however can be risky due to limited amount of data set available (3 years). Will shoot up once Brazil’s interest rates goes down.

Verdict: Risky buy

TIMB: A super resilient stock, growth stock, currently oversold, and makes for a great dividend play as well (9.42%).

Verdict: Buy

AFYA: HUGE growth potential if Brazil’s inflation rate falls. We’re talking about 3x the growth here. However, do note that this is a small cap stock and can be subjected to huge price movements.

Verdict: Risky buy

=

This article was written and published on 12/2/2024. Please do your due diligence before buying stocks — money is precious and your own hard-earned savings. This article does not serve as as financial advice.

Follow me on Instagram @Wavystonks!

I’m trying to build my portfolio as a finance writer, and I’d appreciate if you could follow my Instagram account @wavystonks, where I analyze and suss out which stocks are the best to buy according to financial ratios and trends. See you there!